peepo

Overview

Joby Aviation (NYSE:JOBY) is an eVTOL (electrical vertical takeoff and touchdown) firm much like Archer Aviation (ACHR). Additionally like Archer, it’s a very early-stage firm that’s nonetheless growing its plane and in search of certification from the Federal Aviation Administration.

Based in This autumn 2009, Joby went by a number of rounds of elevating capital and entered the general public markets through SPAC merger with Reinvent Expertise Companions in Q2 2021. Notably, the corporate that it merged with was operated by billionaire Reid Hoffman of LinkedIn. This development in its capital construction mirrors that of Archer, which additionally went public through SPAC at across the identical time.

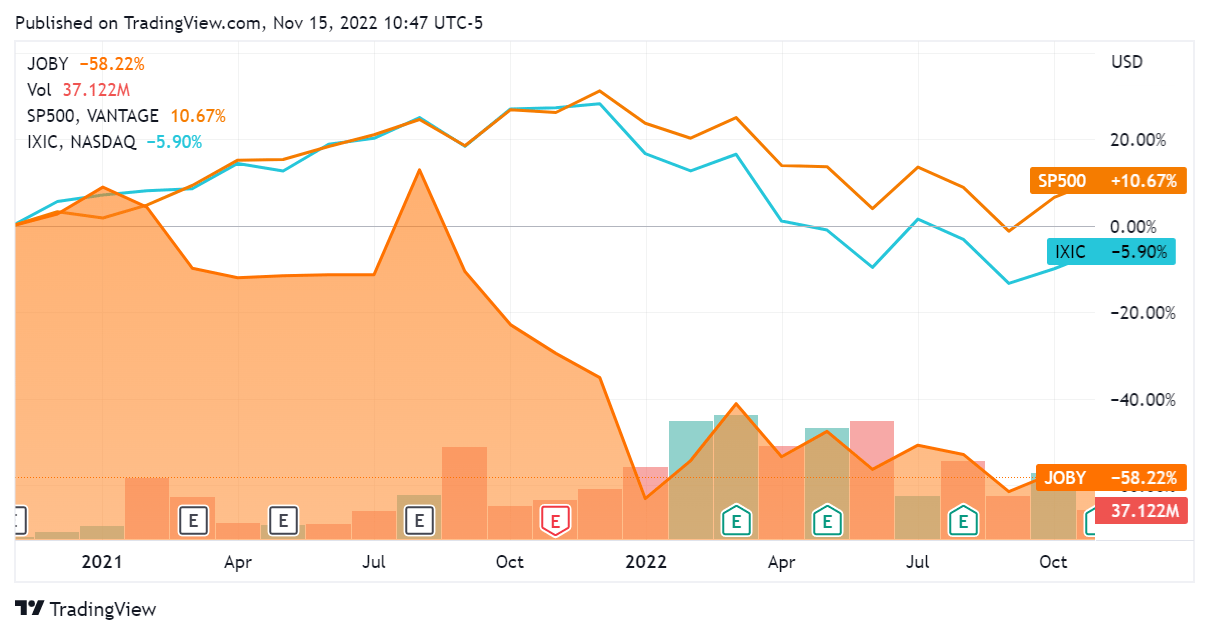

Joby has depreciated considerably since its itemizing, now buying and selling at a 58% low cost. Being a really early-stage development firm, it has displayed downward volatility far past that of the SP500 & NASDAQ composite.

SeekingAlpha.com JOBY 11.15.22

Since I lately posted an article about Archer Aviation, this text will comply with an identical path when it comes to reviewing the corporate’s progress in direction of attending to market in addition to its monetary state of affairs at current. Notable factors of comparability between the 2 firms will likely be highlighted.

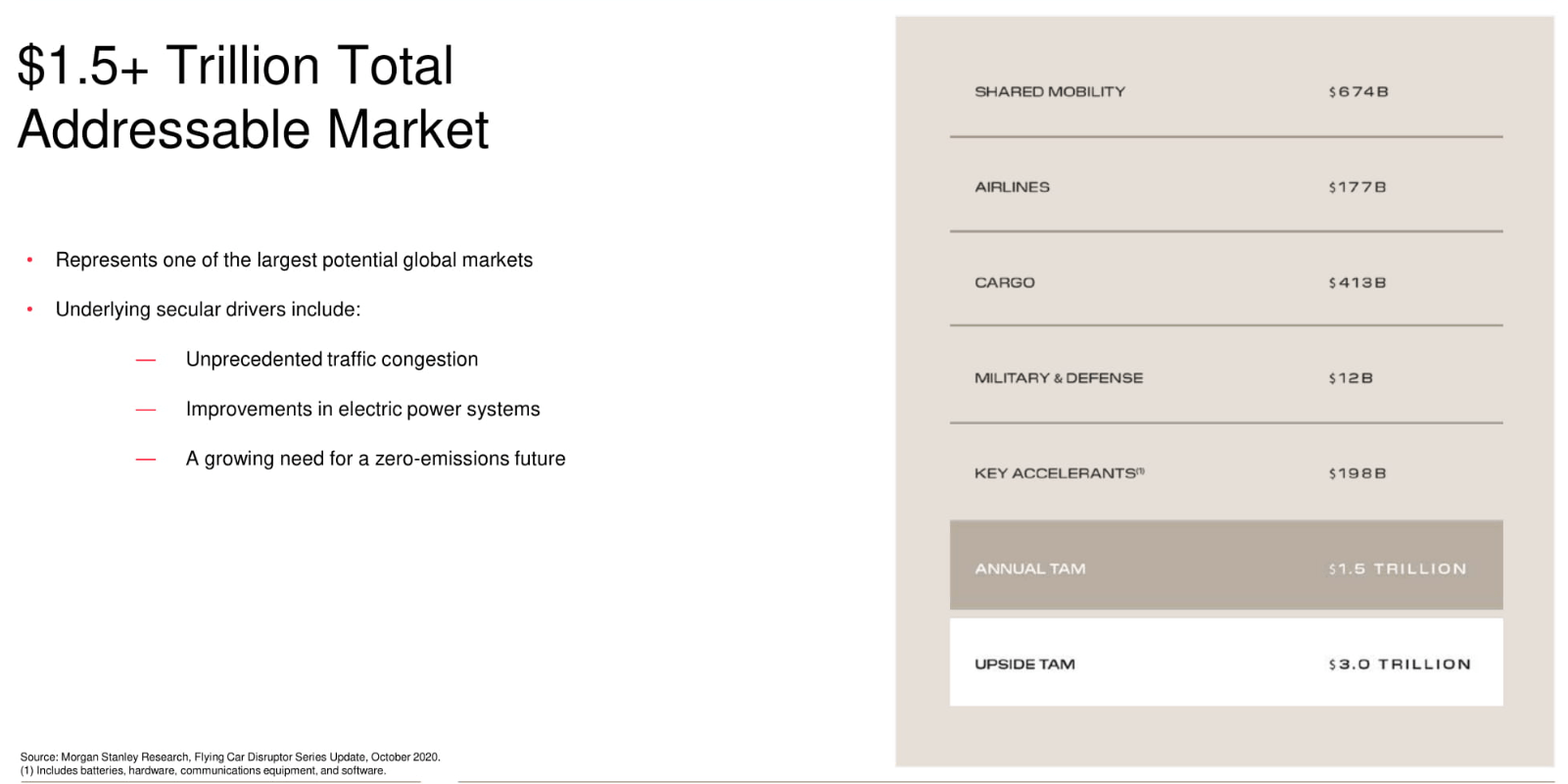

The enterprise fashions between the 2 firms are functionally similar: making a flying rideshare service whereas additionally working as a vertically built-in eVTOL plane producer. As such, the Strategic Assessment outlined in my article about Archer is immediately relevant to Joby, notably together with the $1.5 – $3T eVTOL plane market dimension estimation created by Morgan Stanley.

SEC ACHR Investor Presentation Q1 2021

Financials

Since this firm is a great distance out from income, it is sensible to take a look at it by the angle of a ‘begin up’ and assess its present money place, working expenditures, and financing place.

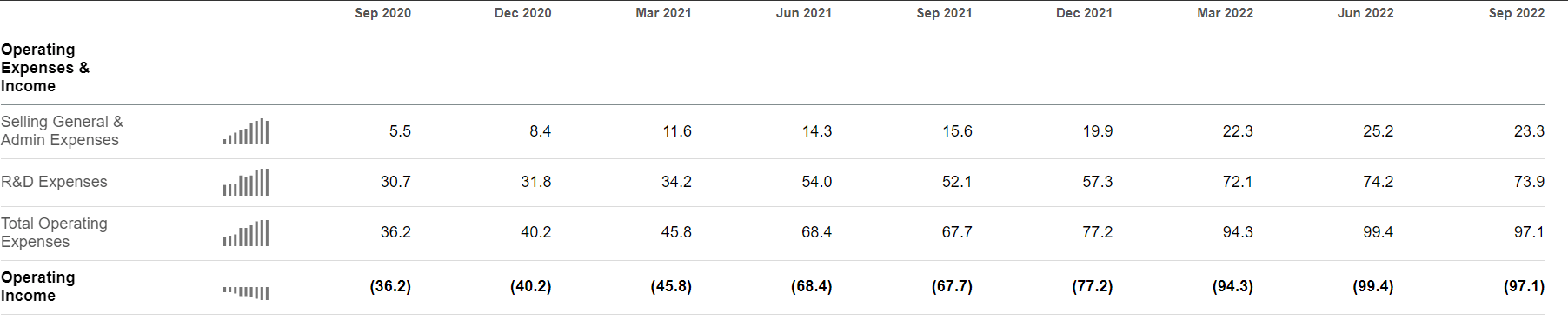

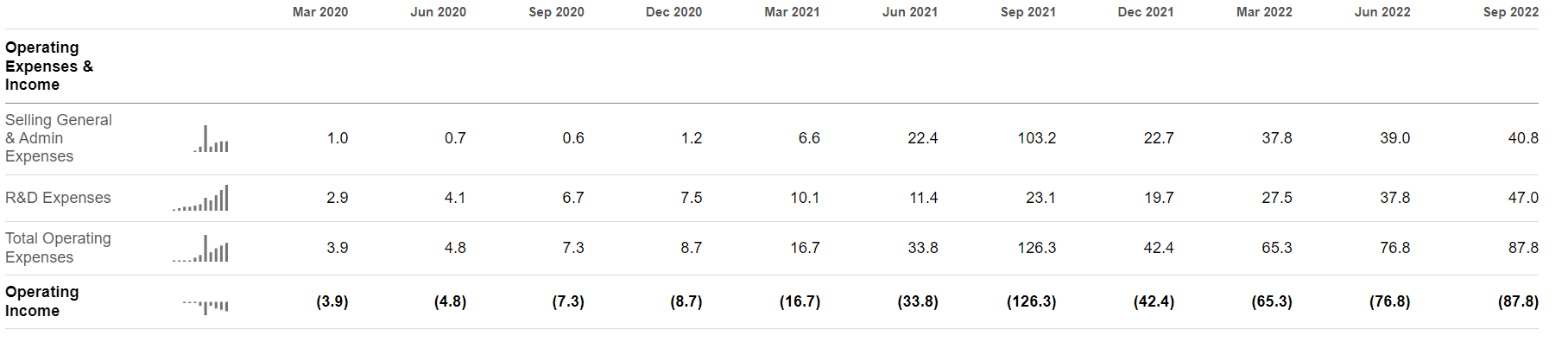

Joby is presently dropping between $90 – $100M per quarter when it comes to working loss, once more mirroring Archer Aviation. Whereas Archer has had a special development as to working loss, one with considerably extra variance, they seem to each have arrived on the identical current ‘regular state’ as to capital expenditures.

Joby

SeekingAlpha.com JOBY 11.15.22

Archer Aviation

SeekingAlpha.com ACHR 11.15.22

Adjusted EBITDA was additionally fairly related between the 2 firms, with Joby’s newest quarter coming in at -$77.7M and Archer’s at -$60.1M. Since these firms are each exceptionally early stage, we will’t be taught a lot from this metric at current.

Each firms have a comparatively wholesome money place that presents a runway for his or her entry into market. Since brief time period investments are thought of readily convertible into money, we will evaluate the 2 firms on the idea of the whole money & short-term investments metric highlighted beneath. Joby at current has 178.9% of Archer’s total money & short-term investments.

Joby

SeekingAlpha.com JOBY 11.15.22

Archer Aviation

SeekingAlpha.com ACHR 11.15.22

This can be a good signal for Joby. Notably, each firms have change into topic to stricter certification necessities by the FAA and have pushed their expectations as to market entry to 2025. Each firms are presently at Stage 2 of FAA compliance certification, though Joby achieved this milestone a full 5 months earlier than Archer did. It’s truthful to imagine that they’ve carried this momentum ahead and proceed to be forward when it comes to certification, however the course of is advanced sufficient to be troublesome to foretell.

Joby has the higher hand by on money by roughly $400M. Apart from this, the monetary image of those two firms is kind of the identical.

Progress

Joby and Archer have each established contracts with airways. The distinction right here is the character of the contracts. Joby established an investor relationship with Delta Airways to the tune of $200M, with $60M already invested and $140M contingent on milestones. Archer, alternatively, has established an early buyer relationship with United Airways for 200 of its plane and an possibility for 100 extra; it is a contingent $1B buy order with a $500M possibility in statements launched by Archer’s administration group.

Since each firms are well-capitalized and have the involvement of billionaires (Reid Hoffman for Joby and Tom Moelis for Archer), I take into account Archer’s buy contract to be far more important than the funding contract that Joby has with Delta. That is true on each a qualitative and quantitative foundation: Archer’s contract is greater than 5x the scale of the one signed by Joby.

The addendum right here is that Joby has additionally been capable of signal a contingent customer contract with the USA Division of Protection, particularly the Air Power. Notably this contract was additionally increased by $45M in Q2 2022, bringing it to $75M and to 250% of its authentic dimension. That is troublesome to match numerically with the order settlement signed by Archer, however the DoD is a deep pocketed buyer that has recognized a big curiosity in eVTOL plane. I take this as an excellent signal for Joby.

Conclusion

Upon assessment, Joby is kind of much like Archer but additionally has a number of achievements that will put it forward of its direct competitor. It has a extra sturdy money place in addition to a contract with the DoD as in comparison with Archer’s contingent buy contract with United Airways. Moreover, it’s forward on plane certification and will get to market sooner consequently.

Each firms in query are charting utterly novel territory and the trail forward has many uncertainties. This makes it troublesome to foretell precisely how issues will play out, and it’s sensible to imagine that they each get to market on the identical time.

Nonetheless, Joby seems to be marginally superior to Archer as to its total image. Given the huge market dimension that the businesses are concentrating on, in addition to the clear differentiation from rivals that each have displayed, I’m bullish on each of them for the long run. This implicates an funding horizon of three full years for market entry after which a decade for profitability/money circulation technology; an funding in both would require endurance on the a part of the investor.

{kind=link}