koto_feja

Shares of neurology spinout Longboard Prescription drugs (NASDAQ:LBPH) have fallen by practically 70% since IPO priced at $16 in March of 2021 (close to the height of the prior bubble in biotech). Share value efficiency is barely unfavorable at -4% for 2022.

Latest Q3 report obtained my consideration as money place of $77M places them at near $0 enterprise worth whereas medical momentum (lastly) seems to be accelerating with wholesome volunteer knowledge for lead drug candidate due this quarter adopted by extra vital ends in sufferers with developmental and epileptic encephalopathies (DEEs) in 2H 23. Moreover, a second intriguing asset for uncommon neuroinflammatory indications seems to enter the clinic within the close to time period.

Given the above, I need to dig deeper and produce this title to the eye of my readers as we resolve whether or not it is a good match for the ROTY (medical stage) biotech portfolio.

Chart

FinViz

Determine 1: LBPH weekly chart (Supply: Finviz)

When charts, readability usually comes from looking at distinct time frames so as to decide vital technical ranges and get a really feel for what is going on on. Within the weekly chart above, we are able to see share value steadily fall from mid-teens to present ranges within the $4 to $5 vary. The inventory has lately jumped above 50 day shifting common and it seems like continuation is feasible into the This fall well being volunteer knowledge replace. With underneath the radar part 3 readout for lorcaserin in DS (dravet syndrome) anticipated in Q2 2023 (Longboard receives 9.5%-18.5% royalties on gross sales), my preliminary take is that traders on this title would do effectively to build up dips within the close to time period.

Overview

Based in January 2020 with headquarters in California (22 workers), Longboard Prescription drugs at present sports activities enterprise worth of ~$8M and Q3 money place of $77M offering them operational runway into 2024. There have been 17.2M shares excellent as of November 1st.

September’s webcast at Wainwright Healthcare Conference offers a superb overview, with CEO noting that Longboard was spun out of Enviornment Prescription drugs (purchased out by Pfizer for $6.7B a yr in the past) in 2020 with concentrate on creating novel CNS-targeted property. Firm has a big G protein-coupled receptor-based (GPCR) pipeline behind it and curiously sufficient, Enviornment (Pfizer) continues to personal 23% of the corporate.

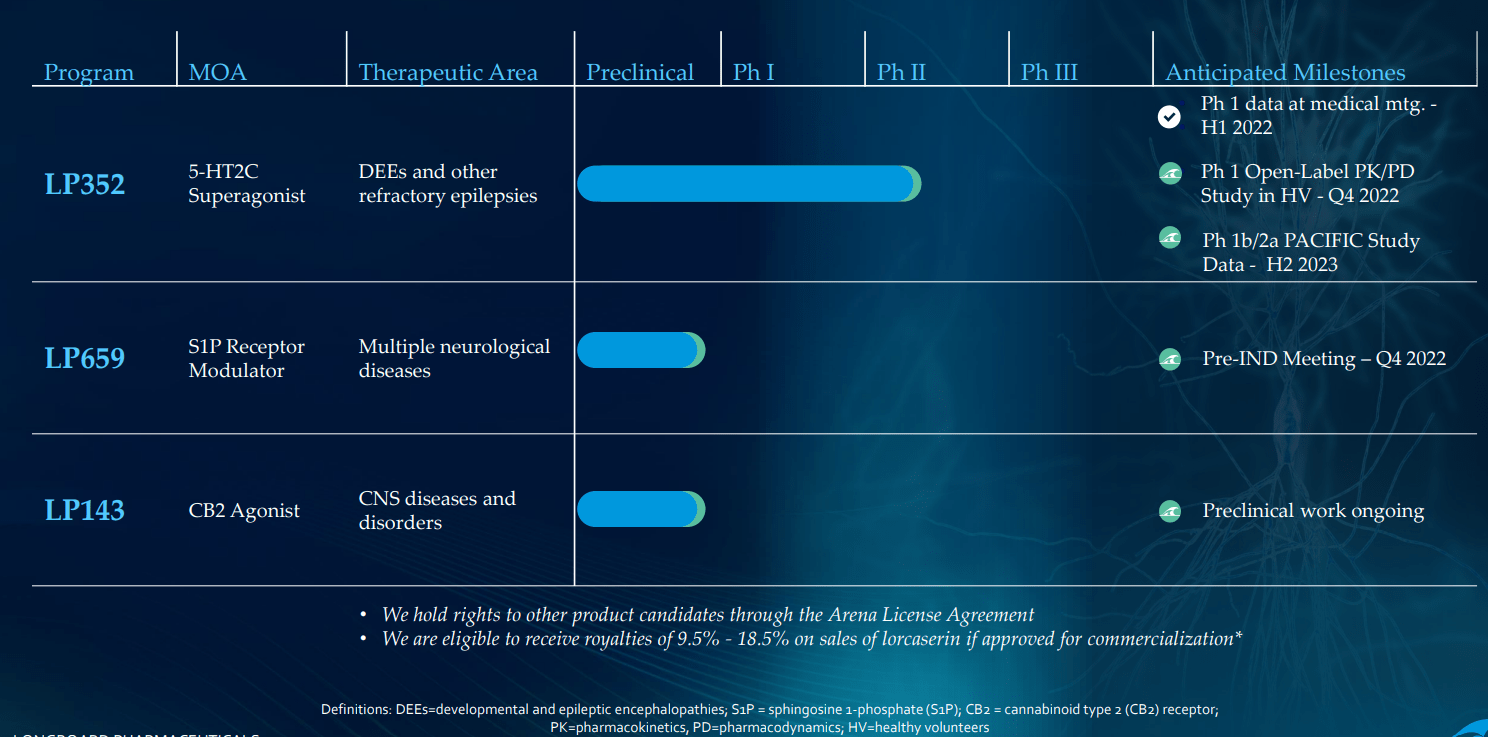

Longboard is concentrated totally on two packages, 5-HT2C agonist LP352 for the therapy of seizures related to DEEs and S1P receptor modulator LP659 with probably broad applicability throughout numerous neurological indications.

Company Slides

Determine 2: Pipeline (Supply: corporate presentation)

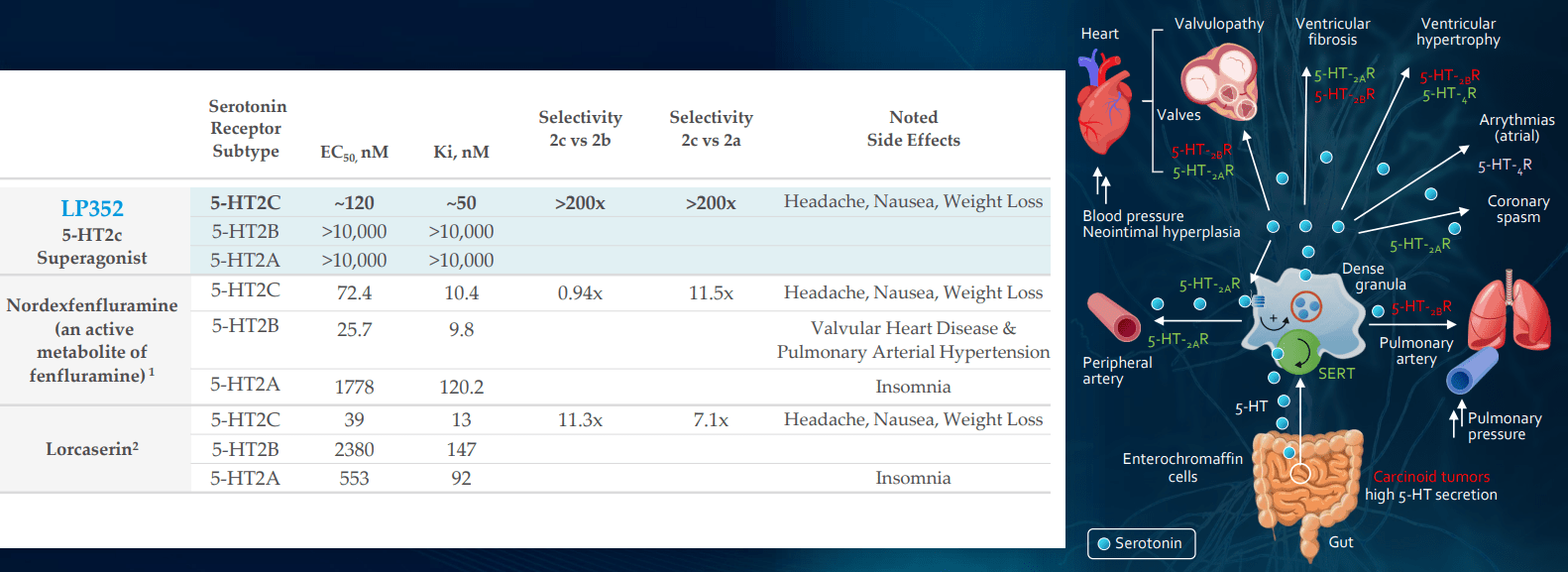

Beginning with LP352, the compound is backed by actual world proof for 5-HT2C agonism displaying exercise throughout a number of sorts of seizures and a number of DEEs. Administration believes LP352 has potential to distinguish from the competitors given excessive selectivity to the 5-HT2C pathway versus A&B (related to unfavorable unintended effects). Moreover, LP352 is the one compound that is been dose-optimized for DEEs and that selectivity might result in cleaner security profile in addition to improved efficacy. Giving it as oral liquid is easiest method for these sufferers.

DEEs (developmental and epileptic encephalopathies) may be regarded as some type of steady seizure dysfunction that proceed all through the lifetime of those youngsters and younger adults and are both syndromic or genetic (particular causal mutation). At the moment there are round 25 recognized DEEs with increased quantity to be characterised sooner or later due to elevated genetic testing.

Company Slides

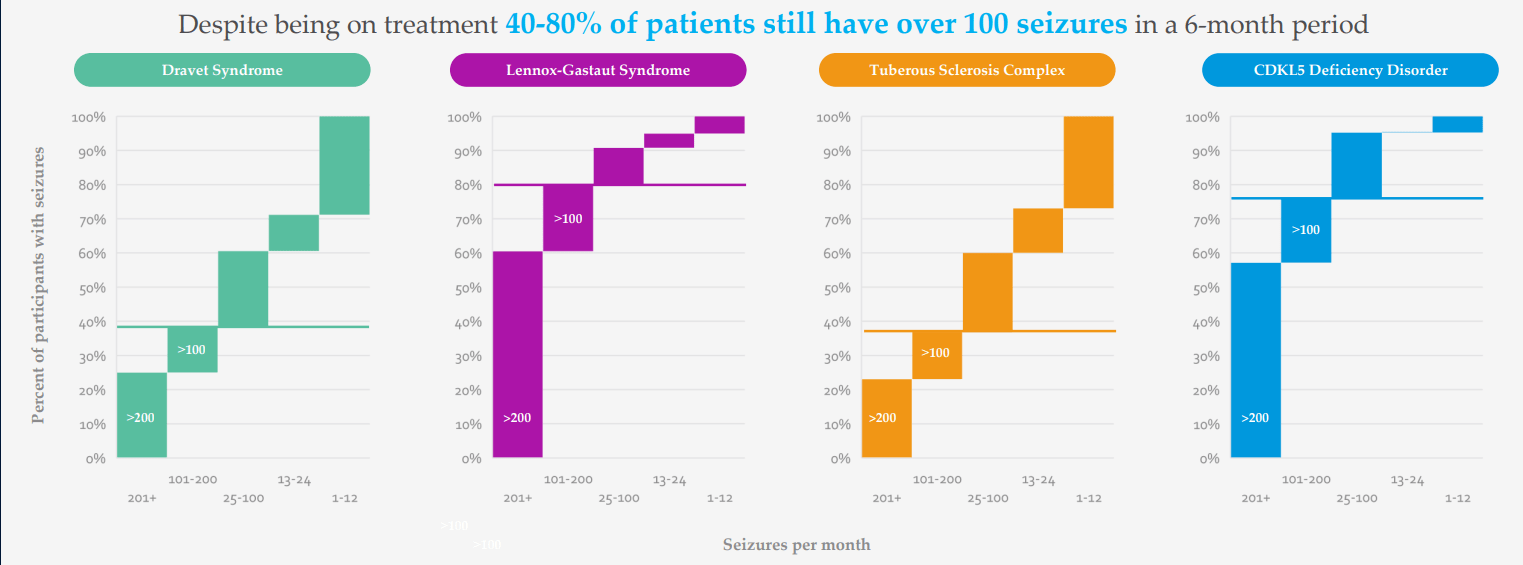

Determine 3: Excessive unmet want in DEEs as mirrored in seizures per thirty days regardless of a number of therapy choices being obtainable (Supply: corporate presentation)

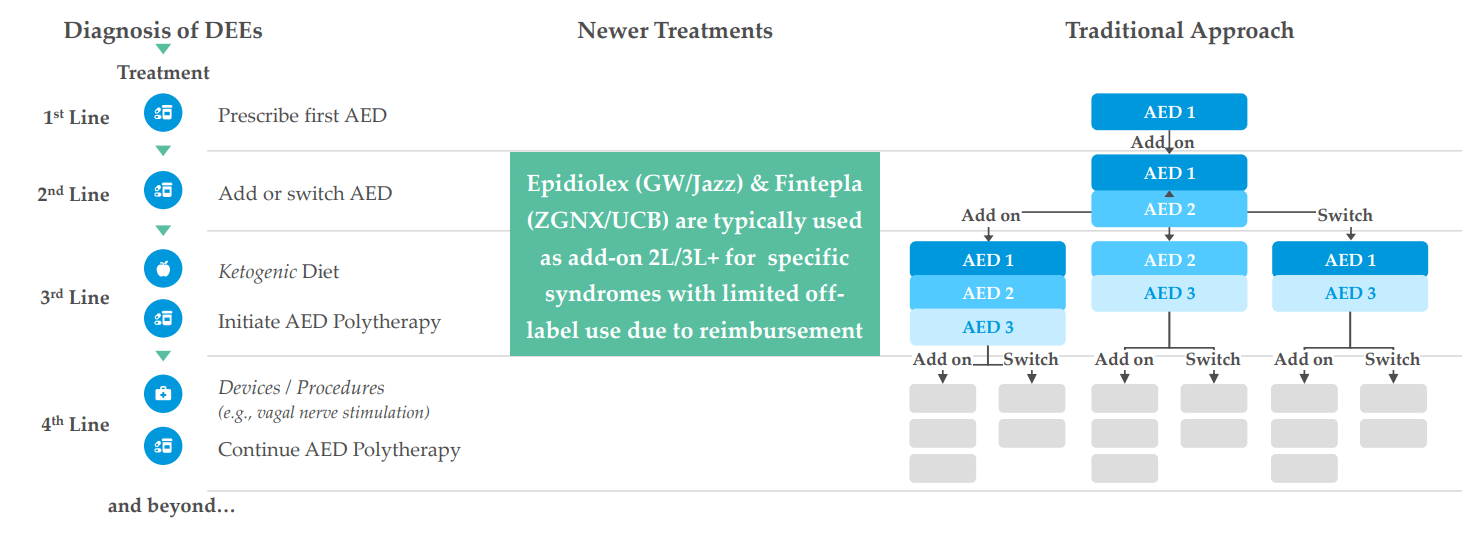

There are 20,000 Dravet sufferers, 50,000 LGS sufferers and 1,500 sufferers with CDKL5 (extra missed and undiagnosed on the market as effectively). They see LP352 as a possible antiepileptic therapy that would have broad utilization throughout numerous the DEEs (why they’re working a basket research). Present therapy paradigm for sufferers is a polytherapy method, placed on a number of AEDs (antiepileptic medication) and varied medication are tried throughout course of therapy. Fintepla and Epidiolex are typically added in 2nd and third line, and long-time readers would possibly recall my prior Purchase suggestions on corporations that purchased these remedies ahead (Zogenix acquired by UCB for $1.9B and GW Prescription drugs purchased out by Jazz for $7.2B). Physicians are in search of remedies which are simpler so as to add on to straightforward of care and that is why Epidiolex has had a better launch trajectory than Fintepla, which has a black field warning. I observe that this previous quarter Epidiolex did $196M of sales (up 22%) and is effectively on its approach to reaching blockbuster standing quickly (peak gross sales estimates of as much as $3B).

Company Slides

Determine 4: DEE therapy panorama (Supply: corporate presentation)

Thus, if LP352 is proven to be secure and efficacious, administration believes it likewise has outsized industrial potential (might be used earlier in therapy paradigm in addition to together with Epidiolex).

Section 1 SAD/MAD knowledge was thrilling per administration, as they’ve discovered there isn’t any meals impact (on this inhabitants timing is vital to oldsters and caregivers). In addition they noticed slight will increase in prolactin ranges (biomarker proof for interplay with 5-HT2C receptor) at center doses examined, permitting them to exclude decrease doses as they transfer into clinic and to do narrower band for dose choice for the part 1b/2a program (exclude increased ranges at which no extra prolactin enhance occurred).

Company Slides

Determine 5: Better selectivity and specificity for LP352 ought to lead to cleaner security profile with fewer off-target results (Supply: corporate presentation)

Objective of the part 1b/2a PACIFIC research is to enroll 50 sufferers with DEEs (broad group, not simply Davet or LGS) with 40 sufferers on drug, 10 on placebo. In regard to screening, they may guarantee sufferers have background historical past of motoric seizures (minimal 4 in preliminary screening interval) then go into titration interval (begin at low dose, then can steadily enhance to increased doses of 6 mg, 9mg and 12mg). The hope is that they’ll attain increased doses whereas drug is effectively tolerated, then keep locked in for 60 days and on the finish they do a dose-titration down. Security, tolerability and pharmacokinetics are major endpoints, however one uncommon side of the trial is that efficacy has been moved into major endpoint as effectively (discount in seizure frequency, in search of comparable findings throughout totally different DEEs and see how totally different seizure sorts responded). Such findings ought to support them in powering pivotal part 2/3 program sooner or later.

company slides

Determine 6: Efficacy in DEEs for predecessor lorcaserin partially derisks the mechanism of 5-HT2c agonism with actual world proof (Supply: corporate presentation)

Objective per protocol is 10 sufferers with Dravet, 10 with LGS and smattering of different DEEs within the PACIFICA research (knowledge anticipated 2H 22). As for bar for fulfillment, different medicines are inclined to circle round 30% to 50% discount in seizure frequency (vary they’d be in search of). Administration’s aim is sort of lofty by way of need to construct out past what Fintepla has (simpler so as to add on high of normal of care). In determine 6 above, I contact on how predecessor drug lorcaserin (initially supposed for treating weight problems) achieved 47% to 62% discount in seizure frequency throughout varied sorts of DEEs. As a result of LP352 has increased selectivity on 5-HT2C, the hope is that can translate into even increased efficacy. Apart from extra widespread DEEs, they may even goal to deal with these the place nothing is accessible as Fintepla cannot deal with them (cannot be used off label on account of black field warning). As for the satan’s advocate query of whether or not LP352 would have a black field label as a result of Fintepla has one, CEO responds that FDA will take a logical method primarily based on the info (Fintepla, lorcaserin and LP352 are very totally different compounds). As famous above, 352 interacts with simply one of the vital vital receptors and wholesome volunteer knowledge signifies (to this point) that black field warning wouldn’t be indicated.

They’re additionally working a part 1 CNS PK/PD research attempting to higher perceive receptor interplay and this could present extra perception into mechanism of motion. Fintepla’s knowledge readout in CDKL5 deficiency is anticipated in 2024 and this additionally might present additional proof that this mechanism of motion is working (prior Dravet confirmed ~70% efficacy and LGS had ~35%). That drug would nonetheless have similar black field and REMS program. Enviornment thinks it is an issue to start out with only one indication like Dravet and shifting by way of every indication step-by-step, which is why they selected a basket research as a greater method at drawing conclusions and opening up affected person entry to those compounds. They’re even contemplating a basket design for pivotal trial, however that might require FDA log out.

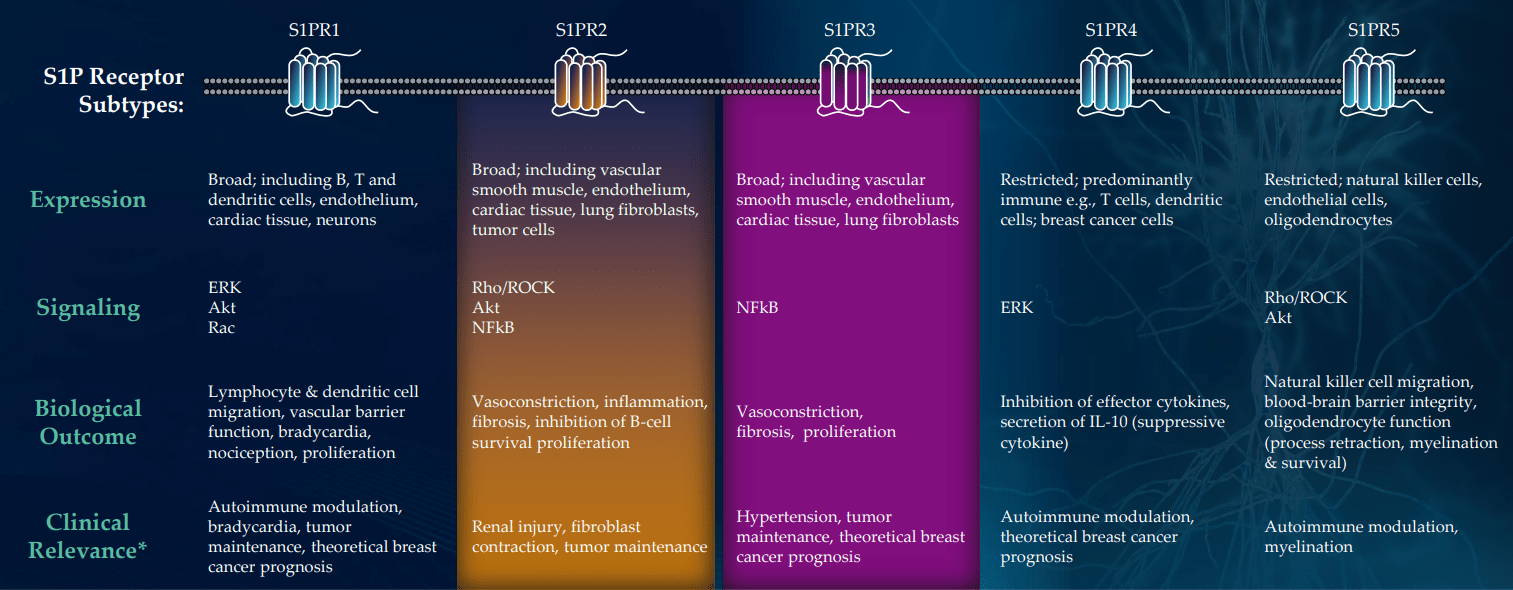

CB2 agonist LP143 isn’t lifeless and has very fascinating preclinical knowledge, however being a small firm with restricted sources administration properly selected to concentrate on preliminary two property (I am glad they don’t seem to be spreading themselves too skinny). IND submission for LP659 (S1P receptor modulator) stays on monitor for the close to time period (“This fall”) with part 1 research to get underway as quickly as attainable after. They’re nonetheless doing a little translational work to find out which neurological illness is smart as a lead indication. For context, there are already a number of S1Ps in the marketplace for treating a number of sclerosis, however 659 has fascinating differentiation together with fast onset of motion and could be very selective to S1P 1 & 5 (doesn’t hit recognized dangerous actors P2 and P3).

Company Slides

Determine 7: Excessive selectivity for S1PR1,5 might lower off-target exercise; S1PR2 & 3 related to severe hostile occasions (Supply: corporate presentation)

Once I consider S1P medication, Novartis’ Gilenya involves thoughts ($3B of peak gross sales) and administration calls LP143 the “cousin of atrasimod”, which was the cornerstone of Pfizer’s $6.7B buyout of Enviornment and recently aced two phase 3 trials in ulcerative colitis (additionally thought to have $3B+ peak gross sales potential). Preclinical mouse mannequin knowledge in MS was fairly promising, however there are already 4 medication permitted for this indication which is why they’re doing work in different ailments.

As for operational runway, they’re guiding for money into 2024 at this level and suppose they’re funded by way of PACIFIC research (seems like increase in Q1 is probably going, in my view).

Choose Latest Developments

In March, the corporate appointed Dr. Randall Kaye as the brand new Chief Medical Officer after Dr. Philip Perrera retired (stayed on in advisory position). Kaye served prior as CMO of Avanir Prescription drugs (purchased out by Otsuka for $3.5B) and Axsome Therapeutics (topic of a recent writeup of mine in consideration for the Core Biotech portfolio).

Different Data

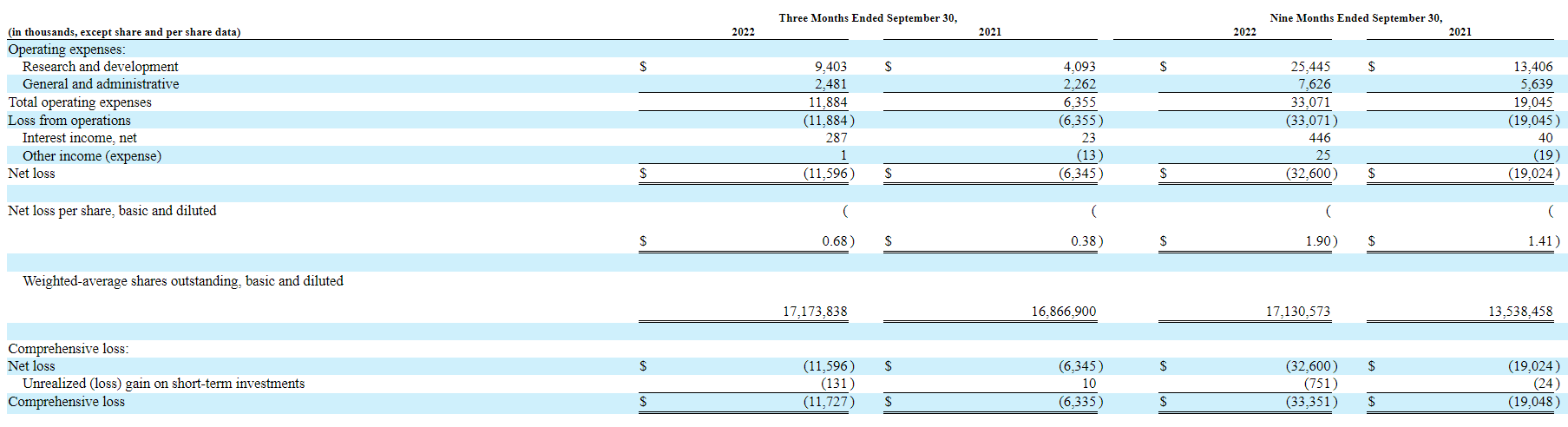

For the third quarter of 2022, the company reported money and equivalents of $77M as contrasted to web lack of $11.6M (which practically doubled from prior yr at $6.3M). Analysis and growth bills rose to $9.4M, whereas G&A was about flat at $2.5M. Developments in development of expenditures appear justified by progress I’m seeing with the pipeline, significantly lead asset in part 1b/2a research.

Quarterly submitting

Determine 9: Govt compensation (Supply: quarterly filing)

Once more, the corporate is guiding for runway into 2024 however I nonetheless suppose we see a dilutive financing within the subsequent quarter or so. Gathered deficit since inception of simply $42M speaks effectively in regard to administration’s stewardship of the stability sheet and preserving expenditures at an affordable degree.

As for competitors, Jazz Prescription drugs (JAZZ) Q3 commentary on Epidiolex replace is useful for context by way of what we might see for LP352 IF it is proven to be secure and efficient (vital to not get forward of ourselves). Jazz’ administration notes that Epidiolex is seeing development pushed by underlying demand and is poised to turn into a cornerstone of therapy for refractory seizures. Market analysis signifies practically 60% of prescribers are shifting Epidiolex up within the therapy algorithm (synergistic results with Clobazam, one of the vital extensively used anti-seizure therapies). As Longboard’s workforce talked about in prior presentation, competitors from different modalities resembling ASOs (antisense oligonucleotides) and gene remedy is in very early phases the place promising efficacy has not been demonstrated as of but. This makes me consider Stoke Therapeutics (STOK), which recently reported “positive” interim data for its ASO candidate STK-001 within the part 1/2a MONARCH and ADMIRAL medical research throughout a number of doses (20mg, 30mg and 45mg). Whereas the highest of the press launch highlights the 55% median discount from baseline in convulsive seizure frequency amongst sufferers handled with 3 doses of 45mg, buried underneath that could be a potential security sign of elevated protein within the cerebrospinal fluid that would correlated with month-to-month CSF dosing (27% of sufferers experiencing delicate to average drug-related treatment-emergent hostile occasions). Likewise, non-human primate persistent toxicity research revealed longer than anticipated half-life and slides (to my eyes) put a number of effort into knowledge mining (by no means a great signal). They’ve extra increased dose (45mg and 70mg) knowledge coming in 2023, however at these ranges I’m involved about elevated issues of safety.

As for institutional investors of note, Enviornment/Pfizer owns practically 1 / 4 of the corporate with 23% stake. Cormorant Asset Administration is maxed out with a 9.99% stake and Farallon Capital Administration owns a 6% stake. It is price noting that by way of insiders, President and CEO Kevin Lind has pores and skin within the recreation and owns over 348,000 shares.

As for related management expertise, President and CEO Kevin Lind served prior as EVP & CFO at Enviornment Prescription drugs. On the board of administrators, we discover Vincent Aurentz (prior EVP and Chief Enterprise Officer of Enviornment) and Corinne Le Goff (prior Chief Industrial Officer of Moderna).

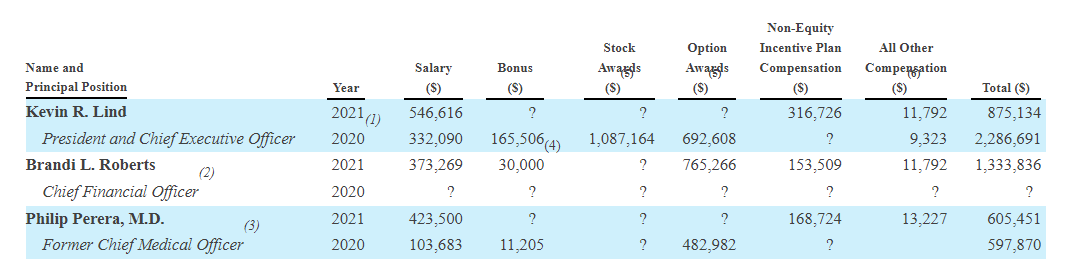

Transferring on to government compensation, money portion of salaries seems fairly affordable for an organization this dimension as do inventory and choice awards (nothing stands proud as extreme).

Proxy Submitting

Determine 9: Govt compensation (Supply: proxy filing)

In regard to IP, for LP352 Longboard owns unique worldwide license to issued and pending claims together with for composition of matter (estimated expiration 2036, not considering time period adjustment or extensions). LP659 patents together with compositions of matter and strategies of therapy are able to persevering with into 2029 (appears on the brief finish to me). Likewise, for LP143 issued and pending patent claims are able to persevering with into 2030.

As for different helpful nuggets from the 10-Okay submitting (it is best to all the time scan these in your due diligence as many corporations like to comb undesirable components underneath the rug), one lesser-known element is that Enviornment license settlement includes mid-single digit royalty on web gross sales to Enviornment/Pfizer.

In reference to Fintepla (fenfluramine) as offering validation for novel MOA in epilepsy (focusing on 5-HT2c receptors), I observe that the drug candidate was initially developed as monotherapy therapy for grownup weight problems in addition to together with phentermine (fen-phen). Reviews later had been printed documenting instances of valvular coronary heart illness and pulmonary arterial hypertension, inflicting the drug to be pulled from the market in 1997. Zogenix efficiently developed fenfluramine for Dravet, BUT acquired black field label for the aforementioned off course results. Equally, Enviornment’s 5-HT2c agonist lorcaserin offers validation for the category and was additionally initially developed for weight administration and marketed as Belviq. It too was pulled off the market following FDA evaluation of upper fee of whole most cancers diagnoses (not statistically important) within the CAMELLIA-TIMI 61 medical research (to my eyes not important at 7.7% versus 7.1% for placebo). A observe up retrospective research in 35 refractory epilepsy sufferers achieved 50% discount in imply month-to-month frequency of seizures in LGS sufferers, 43% discount in Dravet and 23% discount in different epilepsies (Determine 6 above). Following FDA session in 2020, Esai initiated a part 3 research of lorcaserin in sufferers with Dravet syndrome and I reiterate that ought to it’s profitable with Q2 knowledge, Longboard can be eligible for 9.5% to 18.5% royalties (not a small quantity for an organization this dimension).

Remaining Ideas

To conclude, with market capitalization of $85M and EV of $8M, valuation of Longboard Prescription drugs seems exceedingly low cost in comparison with market alternative and excessive unmet want in treating DEEs regardless of lately permitted remedies like Fintepla or Epidiolex. Regardless of LP352 being an early-stage asset, important derisking has taken place through wholesome volunteer knowledge and prior validation for MOA of 5-HT2c agonism through Fintepla’s approval along with lorcaserin’s proof-of-concept knowledge. It is smart {that a} extremely selective compound with improved security & tolerability profile would enable for using increased doses to probably obtain even larger efficacy.

Buyers will not have to attend lengthy for needle shifting catalysts, as part 3 knowledge for lorcaserin in Dravet is anticipated in Q2 (major completion date of March eighth per clinical trials website). Equally, knowledge from the PACIFIC basket research of LP352 in a number of DEEs is anticipated in This fall.

For readers who’re within the story and have finished their due diligence, LBPH is a Purchase and I counsel initiating a pilot place within the close to time period. A prudent technique might be to buy half of desired publicity presently, then ready for dilution or the lorcaserin part 3 readout earlier than taking additional motion.

I want to warning readers that buying and selling quantity for the inventory is low at common day by day quantity of 21,000 shares (~$100,000 price). Thus, restrict orders are a should and I counsel spacing out one’s purchases over time in smaller orders.

From an ROTY perspective (concentrate on subsequent 12 months), I’m not at present contemplating this one for near-term entry given market capitalization is underneath our $100M restrict and extra importantly the inventory is thinly traded with low quantity inflicting huge bid-ask unfold. That might change within the subsequent couple quarters when needle-moving readouts are nearer.

One key threat is critical dilution inside the subsequent quarter or two, contemplating the corporate has money runway of simply 1 yr or so. Delays within the clinic would equally punish share value and valuation, as it could imply present money place is insufficient to achieve the PACIFIC readout. Upcoming knowledge units together with lorcaserin part 3 and LP352 in PACIFIC research might show disappointing, whether or not from security perspective (revealing tolerability issues or off course toxicities) or efficacy (not excessive sufficient to point out differentiation versus predecessor medication). This for all functions may be thought-about a single-drug firm for the current till part 1 knowledge is reported for S1P receptor modulator LP659 in 2024 or so. One other satan’s advocate level is whether or not Pfizer will proceed to personal its 23% stake or promote it sooner or later (which might put stress on share value as effectively). Once more, LBPH is a small firm at sub $100M market capitalization and so readers ought to anticipate elevated threat and volatility right here.

Writer’s Notice: I vastly recognize you taking the time to learn my work and hope you discovered it helpful. Whereas I submit analysis on many corporations that curiosity me, in ROTY (medical stage) and Core Biotech (industrial stage) portfolios I personal simply 15 or fewer names so as to concentrate on tales which are highest conviction for me.

{kind=link}