[ad_1]

Regardless of the vagaries of day-to-day market motion, the goal for buyers will stay the identical because it at all times has been: To search out shares that promise profitability, and a constructive return going ahead. Whereas troublesome to search out in in the present day’s inflationary atmosphere, worthwhile shares are nonetheless the trail to profitable investing.

Protecting the Chinese language car marketplace for Singapore banking big DBS, analyst Rachel Miu sees a chance for income within the Asian electrical car (EV) area of interest. China has taken a full-on method to encouraging adoption of EVs, and the nation boasts numerous modern automotive makers centered on electrics.

Miu has picked out two EV shares as probably candidates for a flip towards profitability as early as subsequent yr. We’ve used the TipRanks platform to examine the small print and discover out what else makes them interesting funding decisions. Let’s take a better look.

Li Auto Inc. (LI)

Li Auto is likely one of the main corporations in China’s EV sector, and has specialised within the EREV area of interest, or prolonged vary electrical autos. These autos use a spread extender – a small engine – to maintain the electrical system charged. Li has leveraged this know-how to provide a line of electrical SUVs, designed for the household market. The corporate, which was based in 2015, started serial manufacturing in 2019. As of November 30, Li has delivered a complete of 236,101 autos, and is engaged on a battery powered design.

This previous December 1, Li introduced its November supply replace – a complete of 15,034 within the month, for an organization document, and up 11.5% year-over-year. Li’s Li L9 mannequin, a full-size 6-seater, cleared the path within the firm’s deliveries and was the best choice, nationally, in its class. Li additionally reported having a large community to assist its autos, with 276 retail shops in 119 cities, and 317 service facilities in 226 cities.

Additionally this month, Li reported its monetary outcomes for 3Q22. Beginning with deliveries, the corporate reported a 5.6% year-over-year improve, to 26,524 deliveries for the quarter. This supported a complete income of $1.31 billion, of which $1.27 billion got here from car gross sales. The highest line was up 20% y/y. Li noticed a internet lack of $231.3 million in Q3, together with a money burn of $71.5 million.

Regardless of the excessive internet loss, firm administration is sanguine about profitability going ahead, saying {that a} mixture of elevated manufacturing, environment friendly execution, and price administration has the agency on observe ‘to hit our profitability inflection level.’

DBS’s Miu agrees that Li has a lot going for it and in addition believes the corporate is heading for its first worthwhile yr. She writes, “Li Auto is the primary auto OEM to leverage EREV know-how to interrupt into the extremely aggressive EV business with a sterling gross sales efficiency, regardless of a brief working historical past. The corporate goals to launch its first battery electrical car (BEV) mannequin in 2023, creating its second long-term progress pillar… The corporate is predicted to show worthwhile in FY23 – the primary amongst pure EV start-ups in China.”

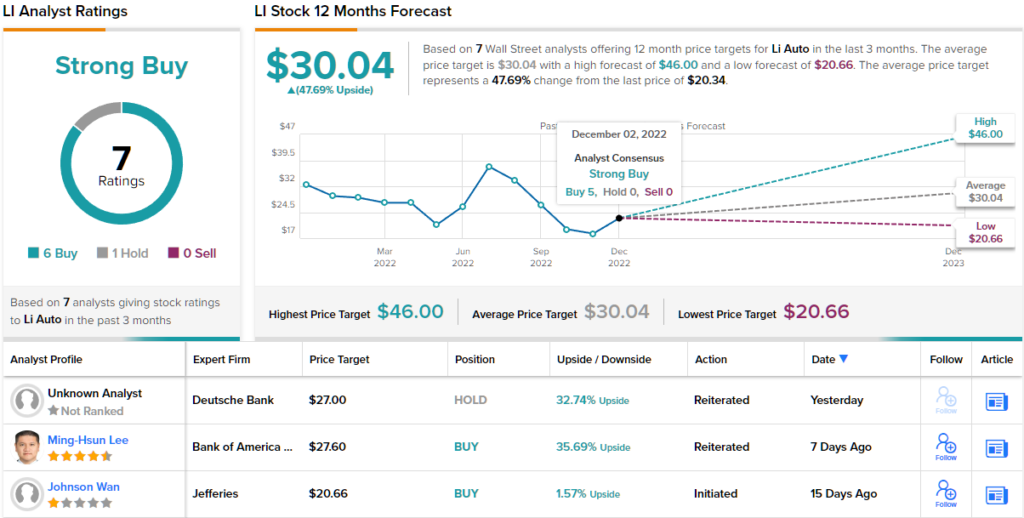

Trying ahead, and placing some numbers behind her feedback, Miu charges the shares as a Purchase and units a worth goal of $29, suggesting a one-year upside potential of ~43%. (To look at Miu’s observe document, click here)

Total, there are 7 latest analyst critiques on file for Li Auto, they usually embody 6 Buys towards a single Maintain for a Sturdy Purchase consensus score. The inventory is promoting for $21.36 and has a $30.04 common worth goal, implying a acquire of ~48% within the yr forward. (See LI stock forecast)

Nio, Inc. (NIO)

Subsequent up is Nio, one other of China’s main EV corporations. Nio has been engaged on battery-powered EVs from its starting, and has been making car deliveries since 2018. At present, the corporate has 6 client fashions in the marketplace, together with sedan, coupe, and SUV designs. Along with car manufacturing and supply, the corporate additionally options the NioPower division, providing Batter-as-a-Service for EV house owners. BaaS applies the favored ‘as-a-Service’ mannequin from the software program world to car {hardware}, permitting clients to decide on quick, economical choices for swapping out complete battery packs and maintaining their autos totally charged.

Final month, Nio reported stable supply numbers, of 14,178 autos for November and 106,671 for the primary 11 months of 2022. These numbers represented y/y positive aspects of 30% and 31% respectively. Because it commenced car deliveries, Nio has delivered a complete of 273,741 EVs.

The excessive November supply numbers got here on the heels of stable 3Q22 numbers. The corporate noticed a prime line of $1.83 billion for the quarter, up 38% year-over-year and 24% sequentially. The Q3 prime line was supported by quarterly car deliveries totaling 31,607, up 29% y/y. Q3’s deliveries included 22,859 SUV fashions and eight,748 electrical sedans. Regardless of the stable revenues, Nio is at present working at a loss, of 30 cents per diluted share.

Whereas Nio has but to indicate a internet revenue, the corporate did flip worthwhile – on the gross stage – way back to 2Q20. Within the third quarter of this yr, the gross revenue got here in at $243.9 million. This was down virtually 13% y/y, however represented a 29% acquire from 2Q22.

In her word on Nio, Miu notes that the BaaS and the ‘sturdy’ design pipeline are each constructive for total revenues. Moreover, the analyst says that we must always count on robust gross sales to elevate profitability going into subsequent yr with the financials enhancing on income and margin growth.

“Whereas the pandemic lockdowns and commodity inflation had affected its 2Q-3Q22 operations,” Miu went on so as to add, “we anticipate FY23F car gross margin enchancment on scale growth and blend enhancement. Moreover, stimulative measures to assist the NEV (new-energy car) auto business is predicted to be constructive on gross sales. Lastly, enhancing provide chain and logistic on auto components and parts ought to smoothen EV manufacturing.”

To this finish, Miu positioned a Purchase score on NIO shares, with a $16 worth goal that signifies potential for ~30% share appreciation over the approaching yr.

All in all, this modern EV maker has picked up 12 critiques from the Wall Road analysts, with a breakdown of 8 Buys and 4 Holds giving the inventory its Average Purchase consensus score. The shares are priced at $12.65 and have a mean worth goal of $16.81, suggesting a 33% upside on the one-year horizon. (See NIO stock forecast)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is rather essential to do your individual evaluation earlier than making any funding.

[ad_2]

Source link