Nigel Stripe/iStock by way of Getty Photographs

From the expertise I’ve generated over time, probably the most ‘boring’ firms are sometimes probably the most enticing and, over the long term, they have a tendency to outperform different alternatives available on the market. One actually nice instance of this that performed out over the previous couple of months may be seen by taking a look at Oil-Dri Company of America (NYSE:ODC), a producer of sorbent merchandise that can be utilized in agriculture, horticulture, animal well being, and extra. Maybe the simplest product to level to with a purpose to illustrate what the corporate does is cat litter. However a few of the firm’s choices are also concerned in rather more thrilling issues like jet gas. Regardless that we’re coping with quite questionable financial situations, the corporate’s monetary efficiency as of late has been quite strong. Given this efficiency and factoring in how low cost shares nonetheless are regardless of rising materially since I final wrote in regards to the enterprise, I do suppose it nonetheless deserves a strong ‘purchase’ score right now to mirror my view that shares ought to proceed to outperform the broader market shifting ahead.

Stable outcomes

The final time I wrote an article about Oil-Dri was again in August of this yr. In that article, I talked in regards to the firm’s working historical past, even mentioning that a few of the more moderen monetary information had been considerably discouraging. This largely centered round a decline in profitability that the corporate had skilled. Even with that decline, shares of the enterprise had been wanting quite inexpensive. However within the occasion that monetary efficiency was to revert again to what it had been in prior years, I felt as if upside could possibly be significant. Since then, issues have gone fairly effectively. On the again of sturdy gross sales and revenue efficiency, shares of the corporate have generated a return for buyers of 21.8%. That compares to the three% decline skilled by the S&P 500 over the identical window of time.

Writer – SEC EDGAR Knowledge

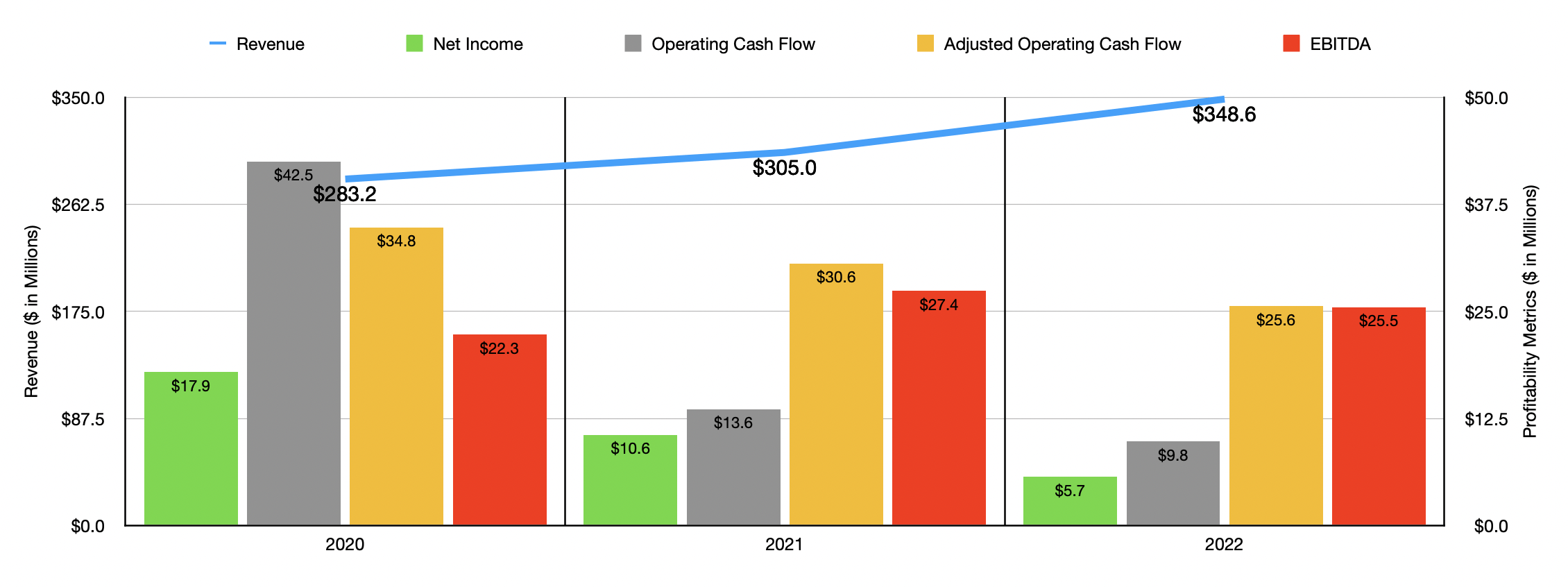

To start out with, we should always contact on how the corporate ended its 2022 fiscal year. In any case, in my prior article, we solely had information extending by the ultimate quarter. For 2022 as an entire, income got here in at $348.6 million. That compares favorably to the $305 million the corporate reported the identical time one yr earlier. However regardless of this rise in gross sales, the corporate noticed its profitability worsen. Internet revenue went from Level $6 million to $5.7 million. Working money movement declined from $13.6 million to $9.8 million. Even when we alter for adjustments in working capital, it might have fallen from $30.6 million to $25.6 million, whereas EBITDA for the corporate declined from $27.4 million to $25.5 million.

Writer – SEC EDGAR Knowledge

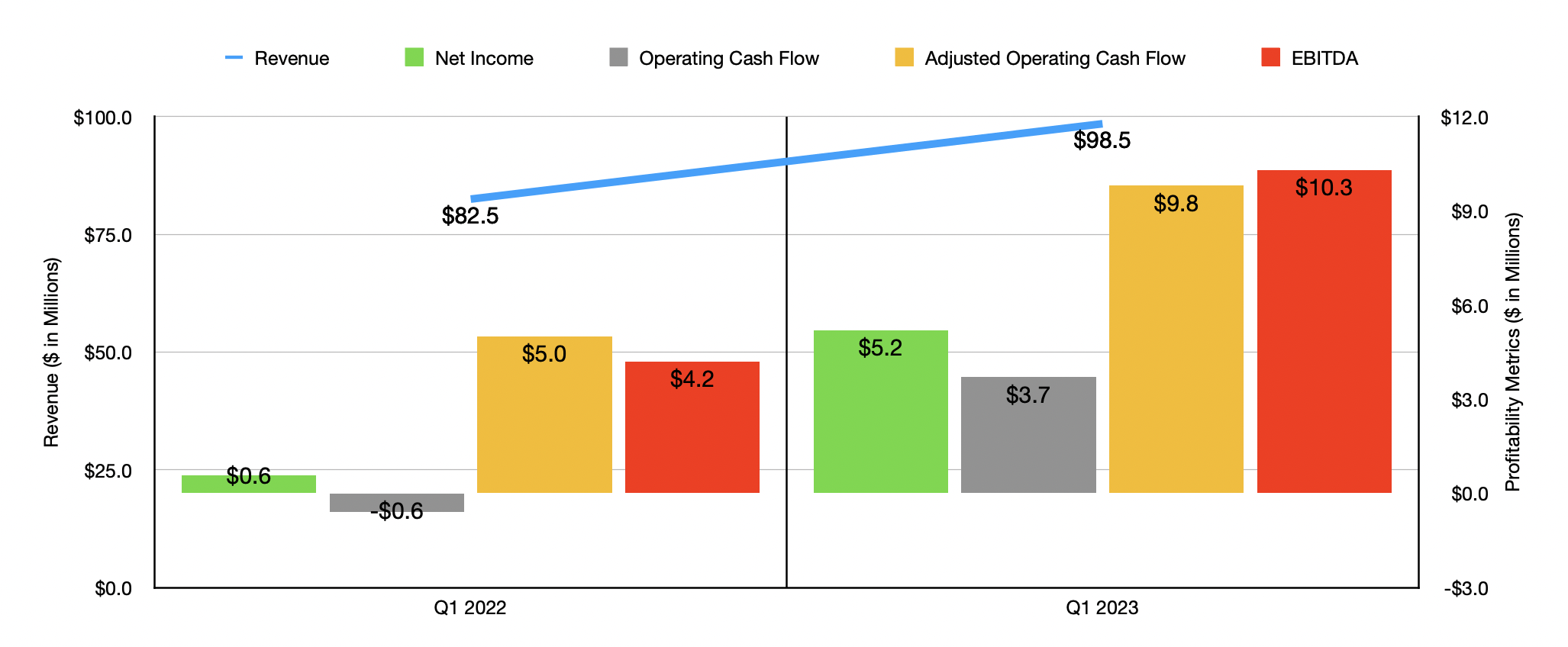

Earlier on this article, I promised you that the image for the corporate was displaying good indicators of enchancment. And I used to be not mendacity. Whereas the 2022 fiscal yr in its entirety was disappointing, 2023 is already wanting up. Within the first quarter of 2023, gross sales for the enterprise got here in at $98.5 million. This 19% improve was pushed by energy throughout each the Retail and Wholesale Merchandise Group, and the Enterprise-to-Enterprise Merchandise Group of the agency. Underneath the Enterprise-to-Enterprise Merchandise Group portion of the enterprise, income jumped 36% because of a 61% rise in agricultural and horticultural chemical service merchandise. Sturdy demand from its prospects, mixed with worth will increase, was instrumental on this regard. In the meantime, underneath the Retail and Wholesale Merchandise Group facet of the enterprise, gross sales rose a extra modest however nonetheless spectacular 12%. In response to administration, greater web gross sales of cat litter, industrial and sports activities merchandise, and different associated choices, had been useful in pushing this income greater. This, in flip, was pushed primarily by worth will increase.

With the rise in income, we additionally noticed profitability surge. The corporate went from producing a web revenue of solely $0.6 million within the first quarter of 2022 to producing a revenue of $5.2 million the primary quarter of this yr. Working money movement turned from unfavorable $0.6 million to a constructive of $3.7 million. And if we alter for adjustments in working capital, then the metric would have practically doubled from $5 million to $9.8 million. An excellent bigger improve may be seen by taking a look at EBITDA, which jumped from $4.2 million to $10.3 million over the course of a yr.

Writer – SEC EDGAR Knowledge

Within the absence of steerage, we do not actually know what to anticipate for the remainder of the present fiscal yr. It’s tempting to venture out outcomes skilled thus far. However given the historic volatility of the corporate’s monetary information and the uncertainty plaguing the market this yr, I feel a greater method is to worth the corporate based mostly on its 2021 and 2022 outcomes. Utilizing information from 2022, shares look remarkably dear on a price-to-earnings foundation, with a buying and selling a number of of 43.2. That compares to the 23.2 studying that we get utilizing information from 2021. However even earnings is probably not probably the most affordable option to worth the agency. Utilizing, as an alternative, the worth to adjusted working money movement a number of, we get a studying of 9.6. That compares to the 8 we get utilizing information from final yr. In the meantime, the EV to EBITDA a number of for the corporate needs to be round 10.5 in comparison with the 9.8 studying that we might get utilizing information from 2021.

As a part of my evaluation, I did examine the corporate to 5 comparable corporations. And a price-to-earnings foundation, these firms ranged from a low of 8.5 to a excessive of 33.9. On this case, Oil-Dri was the costliest of the group. Utilizing the worth to working money movement method, although, we get a spread of between 11.6 and a pair of,411.1. On this case, our prospect is the most cost effective of the group. And at last, utilizing the EV to EBITDA method, the vary was between 9.3 and 49.5. On this state of affairs, solely one of many firms was cheaper, whereas one other was tied with it.

| Firm | Value / Earnings | Value / Working Money Movement | EV / EBITDA |

| Oil-Dri Company of America | |||

| Energizer Holdings (ENR) | 8.5 | 2,411.1 | 10.5 |

| Central Backyard & Pet Firm (CENT) | 14.1 | 22.9 | 9.3 |

| Spectrum Manufacturers Holdings (SPB) | 33.4 | 11.6 | 49.5 |

| WD-40 Firm (WDFC) | 33.9 | 874.2 | 25.1 |

| Reynolds Client Merchandise (REYN) | 25.5 | 21.5 | 17.0 |

Takeaway

For my part, Oil-Dri will not be precisely probably the most secure and enticing firm available on the market. Having stated that, latest monetary efficiency achieved by the agency has been spectacular and shares are buying and selling at very enticing ranges from a money movement perspective. That is true on each an absolute foundation and relative to comparable corporations. Already, the inventory has risen properly since I final wrote about it. Actually, the straightforward cash has already been made. However absent some materials change in enterprise, I do suppose that some further upside could possibly be warranted. As such, I nonetheless suppose that the corporate makes for a ‘purchase’ prospect, even when upside potential won’t be as nice because it was earlier than.

{kind=link}